A settlement check can bring relief, but it can also raise one stressful question: will the IRS take part of it? In most cases, a personal injury settlement is not taxable when it pays for physical injuries or physical sickness.

Still, the answer can change based on what each part of the settlement covers. For example, money for medical bills may be treated differently from punitive damages or interest.

This is why people often ask whether personal injury settlements are taxable before signing papers or filing taxes.

In this blog, you will learn which parts are usually tax-free, which parts may need to be reported, and why the settlement wording matters.

You will also see how the IRS looks at injury payments, emotional distress, lost wages, and medical deductions.

Are Personal Injury Settlements Taxable Under IRS Rules?

Personal injury settlements are generally not taxable under IRS rules if they are tied to physical injuries or physical sickness. IRC Section 104 excludes these damages from gross income, making the nature of the claim the key factor.

The IRS focuses on what the payment is meant to compensate for, not on its label. Compensation for medical expenses, lost income due to injury, and pain related to physical harm typically qualifies for exclusion.

However, payments that serve a different purpose, such as punitive damages or compensation unrelated to physical injury, do not receive the same treatment.

The core rule remains: tax treatment depends on the origin of the claim, not the settlement amount or the wording of the agreement.

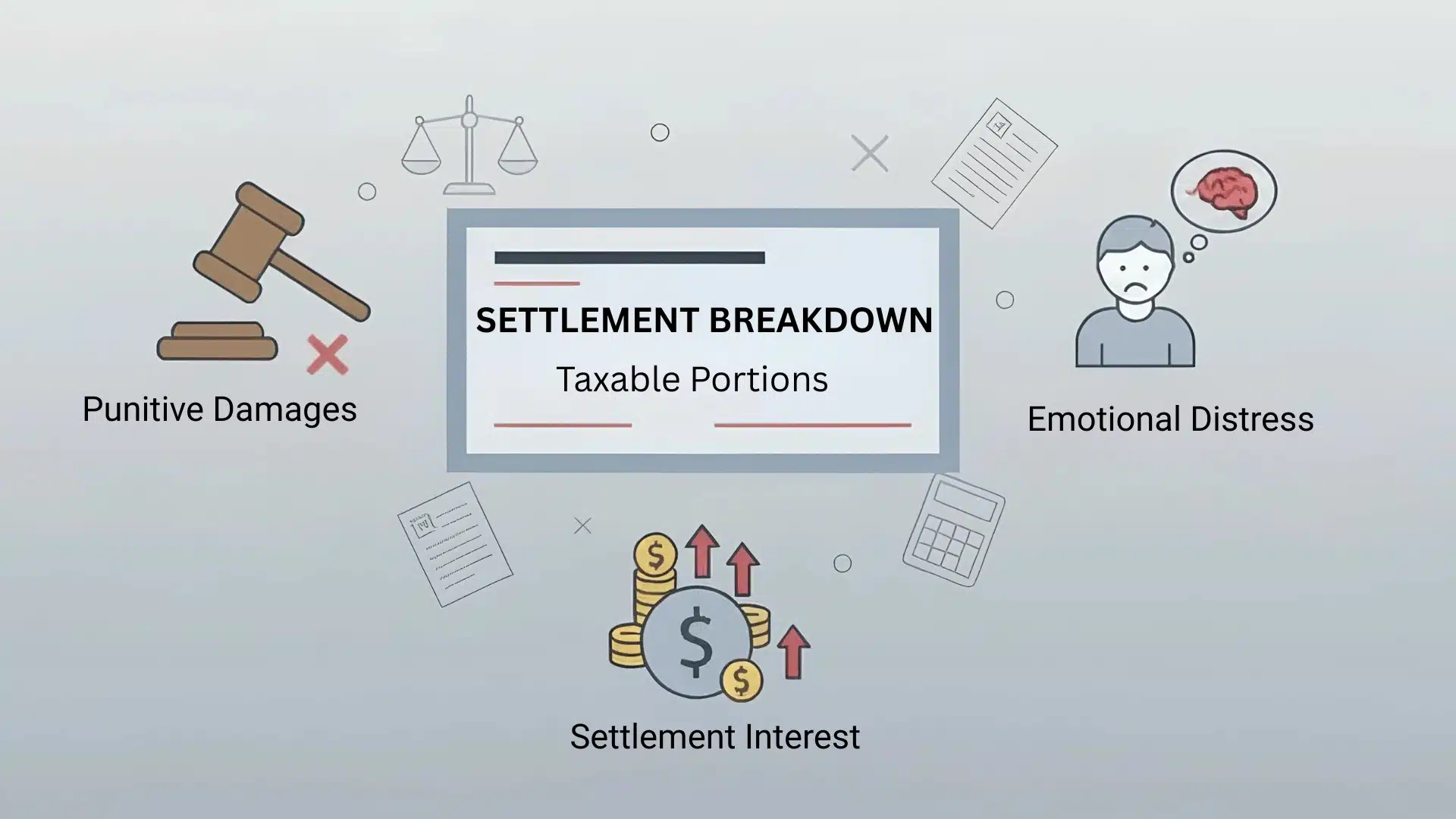

What Part of a Personal Injury Settlement is Taxable?

Understanding taxable components of a personal injury settlement helps avoid surprises at tax time and ensures proper financial planning after receiving compensation.

1. Punitive Damages

Punitive damages are always taxable under IRS rules, and IRC Section 104(a)(2) specifically excludes them from tax-free treatment.

These damages are awarded to punish a defendant rather than compensate for actual losses. Even when linked to a physical injury claim, they do not qualify for exclusion.

Courts often list punitive damages separately in settlement agreements. If not clearly allocated, tax treatment can become a negotiation point. Any amount received is treated as ordinary income.

2. Emotional Distress Not Caused by Physical Injury

Compensation for emotional distress becomes taxable when no physical injury is involved in the claim.

If emotional suffering stems directly from a physical injury, the amount may remain non-taxable. However, cases such as workplace harassment or psychological harm without bodily injury are treated differently.

There is one exception: medical expenses related to emotional distress, like therapy or medication, can be excluded. Only the remaining amount beyond those medical costs is considered taxable income.

3. Interest on a Settlement

Interest earned on a settlement is always taxable, regardless of whether the original compensation is tax-free. This typically occurs when payments are delayed or structured over time.

Courts may award interest, or it may accumulate as part of the agreement terms. The IRS treats this portion as investment-type income, not compensation for injury.

Even if the main settlement relates to physical harm, any interest earned must be reported and taxed accordingly.

What Part of a Personal Injury Settlement is Not Taxable?

A clear understanding of tax-free components in a personal injury settlement helps avoid unexpected liabilities and ensures accurate reporting when compensation is received after a claim.

1. Compensation for Physical Injuries and Sickness

Compensation received for physical injuries or physical sickness is generally excluded from taxable income under IRS rules.

This includes damages from car accidents, slip-and-fall incidents, or medical negligence where bodily harm is clearly established.

The injury must be physical in nature, meaning visible or medically diagnosed harm such as fractures, internal damage, or nerve injuries.

Proper medical documentation strengthens the claim and supports the exclusion during any tax review process or audit.

2. Medical Expense Reimbursements

Reimbursements for medical expenses are typically not taxable, provided the expenses were not previously deducted on a tax return.

If a deduction was taken and resulted in a tax benefit, then the reimbursed amount becomes taxable under the tax benefit rule. This ensures there is no double advantage.

Keeping accurate records of medical payments and prior deductions is essential to determine the correct tax treatment and avoid reporting errors.

3. Lost Wages Tied to a Physical Injury

Lost wage compensation included in a settlement remains non-taxable when it directly results from a physical injury that prevented work.

Although wages are normally taxable, their classification changes when linked to injury-based claims. The origin of the payment determines tax treatment, not the label.

If no physical injury exists, such as in employment disputes, lost wages become taxable. The connection between injury and income loss must be clearly established.

How Do Mixed Settlements Affect Taxes on a Lawsuit Settlement?

Many general guides miss a key detail: personal injury settlements are often paid as a single amount covering different types of damages, and that split affects taxes.

The IRS relies on the settlement agreement to determine how the money is categorized. If the document clearly states that $200,000 is for physical injuries and $50,000 is for punitive damages, that breakdown is usually accepted.

Problems arise when the agreement lists only one total figure. In that case, the IRS has more flexibility to treat parts of the payment as taxable.

This makes precise wording in the agreement extremely important. A skilled attorney negotiates both the total compensation and the definition of each portion.

You can review examples of personal injury settlement amounts to understand how different damage categories typically break down in real cases.

When multiple claims exist, such as physical injury and defamation, each must be assessed separately. The automobile accident lawsuit process often includes several categories, making proper classification essential.

Do You Have to Pay Taxes on a Lawsuit Settlement After Attorney Fees?

This is where the secondary question, “Do you have to pay taxes on a lawsuit settlement?” gets complicated in a way that has caught people off guard since 2018.

Before the Tax Cuts and Jobs Act of 2017, plaintiffs in most civil cases could deduct attorney fees as a miscellaneous itemized deduction. That deduction was eliminated for most types of lawsuits.

The result: if your settlement is taxable, you may owe income tax on the gross settlement amount, even though your attorney kept a significant portion as their contingency fee.

For physical injury cases, this issue largely does not arise because the settlement proceeds are excluded from income regardless.

But for any taxable portion of a settlement, including punitive damages or non-physical emotional distress awards, the attorney fee deduction issue is real.

The average car accident settlement involves primarily non-taxable proceeds, but when punitive awards are part of the picture, the net-after-tax figure can differ substantially from the gross amount.

There are limited exceptions. Attorneys’ fees in employment discrimination cases retain special above-the-line deductibility under IRC Section 62(a)(20). If your claim involves employment rights violations, this is worth discussing with a tax advisor.

When to Consult a Tax Professional After a Settlement?

Not every settlement calls for a tax professional, but some situations make guidance essential.

Advice is recommended when a settlement includes punitive damages, non-physical emotional distress, or reimbursement for previously deducted medical expenses. Unclear allocation within the agreement is another red flag.

Structured settlements add complexity. Payments made over time for physical injuries are generally non-taxable, but any interest earned within the structure may be treated differently depending on the annuity design.

The average wrongful death settlement often uses structured payments, making coordinated legal and tax planning important.

A tax advisor and personal injury attorney should work together when taxable elements are involved. The wording of the settlement agreement directly affects tax outcomes, and fixing issues later can be difficult.

In personal injury litigation in Nevada, the state does not impose its own income tax, so there is no separate Nevada state tax liability to analyze in a settlement. Federal tax law is the only applicable framework.

Conclusion

The IRS rules on personal injury settlements are more favorable than most people expect. Physical injury compensation, medical expense reimbursements, and related lost wages are generally excluded from income.

The exceptions, mainly punitive damages, interest, and non-physical emotional distress awards, are specific enough that a well-structured settlement agreement can minimize or eliminate the taxable portion entirely.

The structure of your settlement agreement is not just a legal formality. It has direct consequences for what you owe at tax time. If your case is still pending, this is a conversation worth having with your attorney now.

If you have already settled and are unsure about the tax treatment, a CPA or tax attorney who handles personal injury proceeds can review your agreement and help you file correctly.

If you were injured in a Nevada accident and have questions about your case or how a settlement should be structured, the team at Mainor Wirth is available for a free consultation. Call today to speak with an attorney about your situation.

Frequently asked questions

Are Workers’ Compensation Settlements Taxable?

Workers’ compensation settlements are generally not taxable under federal law. Payments for job-related injury or illness are excluded from income under IRC Section 104(a)(1). However, if wages are also received while on light duty, that wage portion remains taxable.

Do I Need to Report a Personal Injury Settlement on My Tax Return?

Non-taxable personal injury settlements usually do not need to be reported as income on a federal return. However, taxable amounts, such as punitive damages or interest, must be reported. Review any Form 1099 received to confirm how the settlement is classified.

What IRS Forms Will I Receive After a Settlement?

You may receive a Form 1099-MISC or Form 1099-INT depending on the type of settlement payment. Taxable portions, such as punitive damages or interest, are usually reported to the IRS through these forms. Non-taxable amounts related to physical injuries are generally not reported as income, but reviewing any forms received helps confirm proper classification.

Can a Settlement Be Structured to Reduce Taxes?

A settlement can sometimes be structured to minimize taxable portions by clearly allocating compensation to physical injuries where applicable. The IRS relies on the agreement’s definition of payments. Proper wording and allocation, handled before finalizing the settlement, can influence the overall tax outcome.